Estimation and Budgeting

Lesson Objective

Upon successful completion of this lesson, participants will;

- Learn about the various tools and techniques used for cost estimation and budgeting

- Understand the various components of budgeting

Effort required – 30 minutes

Lesson Introduction

The cost estimates are simply the costs associated with the work packages or activities within the project schedule. Depending on the work package or activity, the cost estimate may be determined using parametric, three-point, or analogous estimating techniques.

It is important for all cost estimates to include any assumptions that were made, where did the estimate originate, who provided the information, level of confidence, etc.

The budget is built using the cost estimates and the project schedule. The budget provides a view of how much the project is estimated to cost both from a total and a periodic perspective. This budget feeds the cost performance baseline which is then used as critical ingredient in performing earned value analysis and other cost management variance analysis techniques.

The project budget must be in alignment with the organization’s funding limits in order to ensure the funding is available and has been appropriated.

Here are the list of tools and techniques used for project cost estimation;

Analogous Estimation

How many of you have taken the effort to see how much was the actual cost of a past similar project or activity , before embarking on a similar new project or task?. I am sure almost everyone would have checked a previous similar work’s cost before estimating the cost of a new similar activity. Estimation based on comparison with a past similar activity is known as analogous estimation. While performing analogous estimation one must validate the similarity of the past similar activity with the task under estimation.

Parametric Estimation

Have you ever heard about the term ‘cost per square feet’?. Cost per square feet is widely used in construction industry. Cost per square feet is calculated by taking an average of the actual cost incurred per square feet from past similar projects. In software testing very often we hear the term ‘Defects per hundred hours of testing’ which is arrived at from historical testing data. Parametric estimation is more accurate than the analogous estimation.

Bottom Up Estimation

As the project progresses, we gain more insight into the projects. When we have sufficient details, we can do the bottom up estimate. That is to say, when we know the activities within a work package, we add up the individual activities estimates and compare with the top down estimate of the parent work package. Then we can add up the work package level costs to arrive at the module level and then to the project level.

Three Point Estimation

From the Optimistic, Pessimistic and Most likely values are estimated, a single point estimate estimate is worked out by applying any one of the formulas;

- (O+M+P)/3

- (O+4M+P)/6

In multiple projects, I have successfully applied combination of Delphi and three point very successfully. Here are the steps;

- Expert team formation

- Shared details of the work

- Team members estimated Optimistic, Pessimistic and Most likely values

- Discussions to arrive at a single Optimistic, Pessimistic and most likely value

- Calculation of single point estimate using either;

- (O+M+P)/3

- (O+4M+P)/6

Reserve Analysis

Unforeseen things happen in projects. There fore one must always account for the unforeseen by adding time and money for contingencies. They are known as management reserves.

Cost Of Quality

Cost of quality (COQ) has two components. The Price of Conformance (POC) include all those activities we are performing to prevent problems from happening. Can you think of some examples?. The costs associated with right recruitment, training, reviews, process definition and implementation etc are examples of POC. The second component, Price of Non Conformance (PONC) contains all those unwanted costs which we could have avoided. Customer complaint handling, deviation from ideal, penalties paid, replacements etc falls into this category. How will the project team treat the COQ elements?. Good project budgets have elements of these factored in.

Type of Project Costs

Cost is classified as direct and indirect costs. Costs directly related to the work packages or activities are direct costs. Direct costs can be further classified into;

- Direct fixed – Direct costs which are fixed. Team’s salary which is not linked to output

- Direct variable – Direct costs which are proportional to the output. Material costs, Team incentives

Indirect costs are further classified into;

- Indirect fixed – Indirect costs which do not change with the output. Project manager’s salary.

- Indirect variable – Indirect costs which changes with the output. Power.

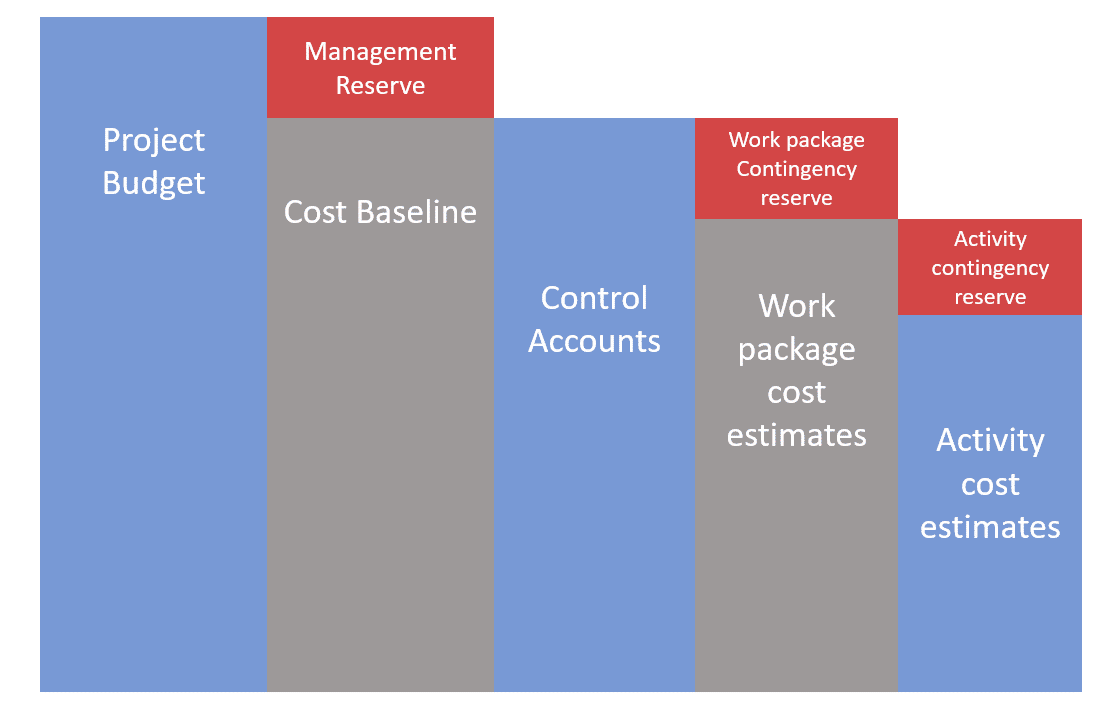

Determining Budget

Cost Aggregation

Now it is time to aggregate the costs and determine the budget. Every task in the project has a cost element and have start and end dates. Bottom up aggregation of cost from the task level to the work package level and to the project level yield the time phased cost budget of the project.

In general, project budget has three components;

- Management reserve – reserved for managing unknown risks. Management has the authority to sanction it.

- Activity / Work package costs – Cost of work. Supervisors have the authority to use it.

- Contingency costs – Reserved for managing known and known-unknown risks. Project manager has the authority to use it.

By factoring in Management reserves and contingency reserves to the cost baseline we arrive at the time phased budget of the project.

Historical Information Review

Historical information provides very valuable insights to estimation. These are very helpful while validating the project budgets. In the construction domain, the budget till foundation work completion is considered as accurate if the budgeted amount till the foundation is within 20% of the overall project cost.

If the requirements and design effort is within 30% of the overall project budget for a software development project it is considered as normal. In matured industries, heuristics are developed based on historical data. These are great inputs to validate time phased budgets.

Funding limit reconciliation

Funding the projects phase wise results in better cost control than end to end funding of the project. Always, the funds dispersed must be proportional to the progress accomplished. Funding risks are addressed better by ensuring that funds dispersed is directly proportional to the Budgeted Cost Of Work Performed (BCWP). In the earned value management vocabulary, budgeted cost of work performed (BCWP) is also known at Earned Value (EV). As a rule of thumb, money dispersed must be proportional to the work completed.

Financing

From where to get the funding is the next challenge. Who will finance the project?. Timely funding is critical to successful completion of the project. Projects can have either a single sponsor or multiple sponsors. Proper financing will prevent projects from lagging behind due to lack of funds during the execution phase.

Summary

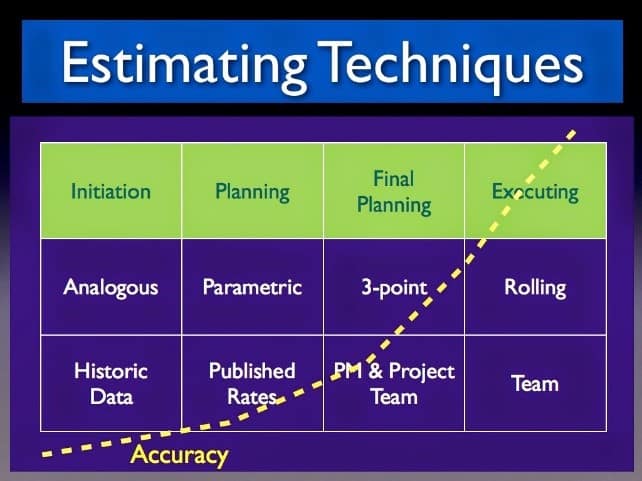

Arriving at the correct budget, management of the budget, ensuring the disbursement of funds based on project progress and then managing the project within the approved budget needs specialized skills, tools and techniques. The most commonly used tools and techniques for estimation are;

- Analogous estimation

- Parametric estimation

- Three point estimates

- Bottom up estimation

- Expert judgment

The diagram below shows the estimation technique, project phase in which it is used and the relative accuracy.

One start with planning for cost management and develop the Cost Management Plan for the project. Actual Estimation of costs is performed by leveraging the detailed work breakdown structure. Once the costs are estimated, they are aggregated to arrive at the cost baseline and then the budget baseline.

Assignment

Estimate the cost of any work package of your project using three point estimate.